US Inflation, Jackson Hole, Fed Chair Jerome Powell and US Interest Rates — What’s the connection to New Zealand?

On Friday evening (26 August 2022) at the Jackson Hole symposium, Fed Chair Jerome Powell gave his much-anticipated speech about the financial markets guidance on the US central bank’s monetary policy tightening plans. The month of August was fraught with market volatility in equity markets, commodities and bond markets as global investors and businesses positioned their chips ahead of the central bank “talk fest” at Jackson Hole.

Fed Chair Jerome Powell’s 8 ½ -minute speech reassured markets that the Fed will keep interest rates in restrictive territory until inflation is brought down to the 2% level. Powell noted that restoring price stability could require a sustained period of lower growth and that labour market conditions will likely soften (i.e., a rise in unemployment will be inevitable). Personal spending figures for July missed expectations, further reducing hopes that the Fed can achieve a soft landing as policy tightens. The Dow plummeted 1,000 points, while the S&P 500 and the Nasdaq tanked 3.4% and 3.9%, respectively.

The upshot, US interest rates will likely be higher for longer and the US will experience a lengthy period of subdued economic growth.

Why was Jerome Powell’s speech and the Jackson Hole symposium so important to the global financial market collective consciousness?

The symposium offsite is essentially a central banker’s annual think tank and a place where most of the world’s central banks can bounce off ideas on how they can effectively do their mandated job, providing their respective economies with price-stability leadership. They all inevitably take a lead from the US Fed. The US still calls the shots of global economic and financial market direction. When the US catches a cold, we all catch the flu and accordingly, the likely medicine to be dished out by the Fed (higher interest rates) will be taken by the rest of us.

Quite simply, markets are very scared that central banks will raise interest rates to such an extent that economic growth is severely compromised. The placement of bets over the past month have been moving backwards and forwards on the likely direction of the Fed on their tightrope walking as they attempt to lower inflation via the blunt tool of monetary policy. The markets are “wishing” for a careful engineering of a soft economic landing through a successful lowering of inflation alongside a limited and short-lived recession.

This is unlikely to mean that interest rates in the US and in other economies such as New Zealand will fall for some time to come (look beyond 2023 and 2024).

Don’t take my word for it. I transcribe some of Powell’s speech below. Make your own judgement call.

· Overarching focus to bring down inflation below 2% (currently 8.50%). Price stability is the bedrock of the economy.

· Burdens of inflation fall heaviest on those who are less able to bear them.

· Bringing inflation down will require forceful use of monetary policy tools and result in a sustained period of below-trend growth.

· There is likely be a softening of labour market conditions.

· Higher interest rates, slower growth and a softer labour market will bring down inflation but will cause pain to households and business. But a failure to provide price stability will cause far greater pain in the long run.

· The US economy is clearly slowing down. Whilst economic measures have been mixed, Powell believes the US economy has good underlying momentum.

· Whilst the lower July monthly readings for inflation were welcome (fall from 9.1% to 8.5%), a single month’s improvement falls far short of the Fed’s requirements.

· Current Fed fund rates (equivalent to NZ OCR) are between 2.25–2.50% and are at the considered long-term neutral level. Likely, the next move will be another large one (i.e., more than 50 basis points).

· In June the Fed’s fund path indicated a rise to 3.75% through to mid-2023. At September meeting, this will be reviewed. (Likely, higher and for longer).

Powell concluded with the following three historical lessons learnt from the high inflation era of the 70’s and 80’s

· Central bankers can and should take unconditional responsibility to deliver low and stable inflation. It is currently a global phenomenon caused by constrained supply.

· Public expectations on future inflation can play an important role in softening inflation over time. The longer that inflation is left unattended, the greater the likelihood that the publics future pricing intentions will be entrenched in their psyche. When inflation is high households and business need to factor inflation into their economic decisions.

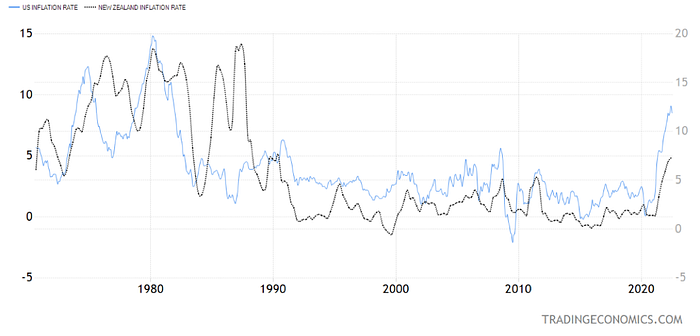

· Must keep at it until the job is done. This may therefore require a lengthy period of very restrictive use of monetary tools. Powell concluded that the Fed’s current objective is to avoid a repeat of the 70’s/80’s by acting now. Note what Powell was referring to in the following inflation and interest rate charts.

The Fed did not finish the job in the 70’s and 80’s taking their foot off the interest rate throttle too early and thereby extending high inflation for longer.

Note how New Zealand inflation is heavily influenced by what happens in the US (US data LHS and NZ data RHS). NZ inflation usually lags US inflation and is mostly higher if you look at the scale. There has been little inflation since the 90’s with brief incursions to 5% in both countries. The 70’s and 80’s is the most telling part of this chart.

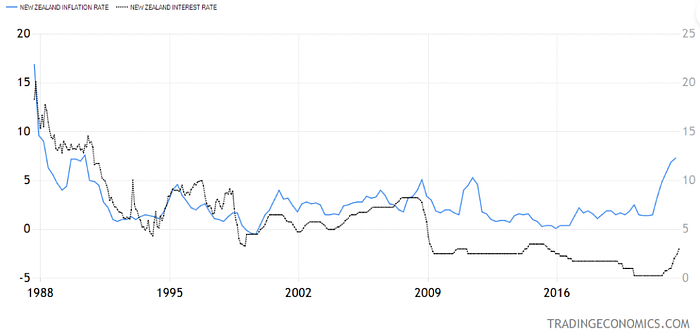

If we accept that New Zealand inflation is likely to materially follow that of the US, then it may not be too much of a stretch to see our interest rates move accordingly.

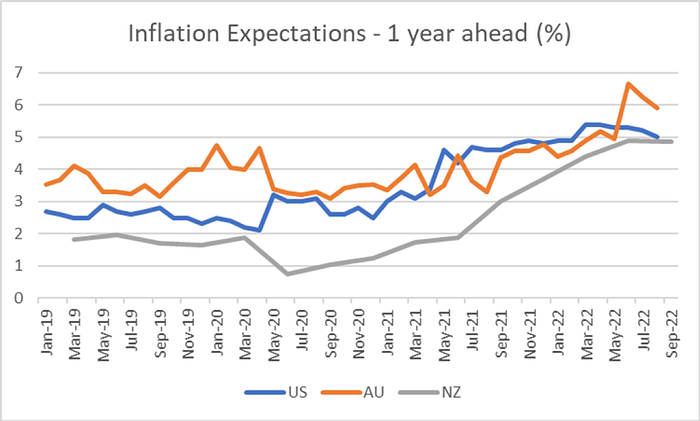

The following chart will be an important measure of how long the central banks may inflict the high interest rate medicine. If expectations trend down, we are more likely to see the foot come off the interest rate accelerator. If they don’t move down in coming months, I cannot see any respite soon.

Economic indicators suggest global activity is slowing, but not collapsing. This has supported the idea that economies have capacity to absorb higher interest rates near-term and the front loading of hikes will bring inflation under control. New Zealand has better experience than most in being able to operate in a high interest rate environment. Prior to the GFC in 2007/8 New Zealand’s long-term average 90-day bank bill rate was 6.50%.

Central banks have a difficult task ahead balancing the risk of persistent inflation with the risk of a recession. A so called “soft landing” (where interest rates are high enough to curb inflation but not cause a recession), is easier said than done especially given the lag between changes in monetary policy and the evidence of its realised impact, the risk of both scenarios is high which makes the soft-landing pathway narrow. This supports why Powell emphasises that they must act now.

Too little monetary policy tightening (interest rate hikes) over the short term and the risk is inflation persists, becoming embedded in expectations and fuelling further inflation — and the result is a need for even higher interest rates and for rates to remain higher for longer.

Too much tightening could push the economy into recession, the trick is to judge a shallow recession and not create a deep and long-term gulley.

Prior to Powell’s speech the market priced the Fed funds path closer to 3.2% and it is highly likely that this will be increased to 4% in coming weeks.

The market also assumed too little monetary policy tightening — underestimating the stickiness of inflation and central bank resolve to take their policy rates into more restrictive territory.

High inflation, high interest rates, softer employment and even softer economic growth could mean higher household and business arrears and loan defaults. This could be a catalyst for increased credit costs and a long overdue corrective return to realistic risk: return links to credit ratings.

Conclusion:

It looks more likely that US interest rates will rise higher and for longer than what the market is pricing in and even with a successful engineering of a soft GDP landing, short-term US interest rates are likely to have a 4 in front and long term (10-year rates) 4.5% to 5%. As the following chart illustrates, where US long-term rates go, New Zealand rates will surely follow (with an added 0.50% -1.00% spread). This suggests that New Zealand fixed-rate mortgages for 2–5 years could build up to a 6.50% -7.50% range over the coming 6 months.

Written by:

Stuart Henderson

Director SRH Consulting

Financial Markets Risk Adviser